by Calculated Risk on 8/20/2025 11:34:00 AM

Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment including multi-family residential.

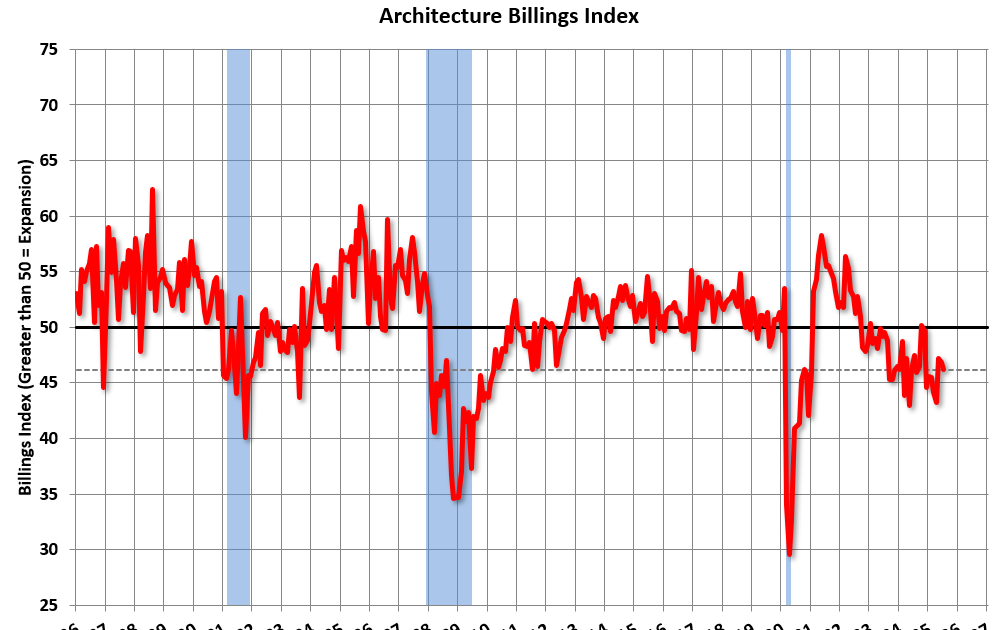

From the AIA: ABI July 2025: Business at architecture firms remains soft

The AIA/Deltek Architecture Billings Index (ABI) score for the month was below 50 for 31 out of the last 34 months, with a score of 46.2, as a majority of firms are still seeing declining billings. There are signs of hope ahead, as inquiries into new work grew slowly but steadily this month, following a brief three-month pause earlier this year. However, the value of newly signed design contracts at firms declined again in July, as firms continue to struggle to convert inquiries into contracts for new projects. This has been an issue for nearly as long as billings have been declining and reflects how soft business has been at many firms over the last two and a half years.

Billings continued to decline at firms in all regions of the country in July. Although conditions in the South looked like they were improving earlier this summer, the share of firms reporting a decline in billings increased this month. Billings remained softest at firms located in the Midwest for the third consecutive month. Business conditions continued to improve at firms with a commercial/industrial specialization this month, where there was nearly an equal share of firms reporting an increase in billings as reporting a decline for the second consecutive month. Firms with an institutional specialization also saw some encouraging signs, although business softened further at firms with a multifamily residential specialization in July.

…

The ABI serves as a leading economic indicator that leads nonresidential construction activity by approximately 9-12 months.

emphasis added

• Northeast (47.8); Midwest (45.1); South (47.5); West (46.4)

• Sector index breakdown: commercial/industrial (49.9); institutional (47.9); multifamily residential (43.7)

Click on graph for larger image.

Click on graph for larger image.

This graph shows the Architecture Billings Index since 1996. The index was at 46.2 in July, down from 46.8 in June. Anything below 50 indicates a decrease in demand for architects’ services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment throughout 2025 and into 2026.

Multi-family billings have been below 50 for 36 consecutive months. This suggests we will some further weakness in multi-family starts.